Russia’s car market still stands to benefit from low saturation. Source: ITAR-TASS

Otto von Bismarck’s observation that Russian cavalry were “slow to saddle up, but ride fast” remains relevant to the country’s automobile industry, which is set to overtake Germany’s to become the largest in Europe in the coming years.

Private car ownership, shunned in Soviet times as an alternative to public transportation, has witnessed an unprecedented boom since the turn of the century with 12 percent growth in 2012 to hit 2.93 million cars sold (marking a full recovery from the 2008 global economic crisis, according to the Association of European Businesses).

This stands in stark contrast to the entire E.U., where sales dropped by 8.2 percent last year to 12 million (the lowest level in 17 years, says the European Automobile Manufacturers’ Association).

The continents biggest market, Germany, dropped by 2.9 percent to 3.08 million cars sold (the difference with Russian sales may be even smaller, according to Ernst & Young, because of dealers registering sales in their own names, reported Bloomberg).

Mercedes ready to start production in Russia

Russia’s automobile recycling fee not to be reduced

Russia’s car market: Too young for crisis

Recent polls predict a bright future for Russia's car insdustry

A major factor contributing to Russia’s automobile boom has been, somewhat ironically, the same high oil prices that have hit American car owners for the last decade. Being the world’s second largest oil exporter, Russians have seen their nominal monthly incomes increase by a factor of 16 in the last decade to hit around $800 last year.

This, coupled with a burgeoning credit market and recovering demographics, has seen the country become Europe’s leading market in everything from cell phones to children’s goods.

And the world’s auto giants took notice. A 30% import duty on new cars (prior to Russia’s WTO ascension last year) – coupled with low duties on parts thanks to state policy aimed at localizing production – favoured the growth of component imports to be assembled locally.

Ford was the first to move in 2002 by opening a $150 million plant in Vsevolozhsk (outside St. Petersburg), followed by Renault (2005), Volkswagen (2007), Toyota (2007), GM (2008) Peugeot/Citroen/Mitsubishi (2010) and Hyundai (2011).

The number of domestically assembled foreign cars sold in Russia increased from 290 thousand (vs. 750 thousand imported cars) in 2007 to 1.22 million (970 thousand imported) in 2012, with the most popular foreign brands being the Hyundai Solaris (110 776 cars sold in 2012), Ford Focus (92 219) and KIA New Rio (84 730) according to the Association of European Businesses.

PricewaterhouseCoopers predicts these figures will hit 1.33 million and 990 thousand this year (for a total predicted market size of $70 billion).

“The myth that Russians mostly drive big jeeps and SUZs doesn’t play out in numbers: the top selling models – both domestic and foreign – are all compact, economical cars,” explained PricewaterhouseCoopers Russia senior manager Sergei Litvinenko.

“But in the last 18 months this segment has stagnated and SUVs have shown the highest growth, especially crossovers like the Renault Duster, thanks to rising incomes and falling technology costs.”

Local Players

However state policies and rising incomes ultimately hit local automobile producers, whose cars are considered by many Russians to be of inferior quality due to outdated assembly technology, run-down fixed assets and poor parts.

Their primary competitive advantage, low prices, has been eroded as increasingly wealthy local consumers have demanded a better product. Sales of new cars under Russian brand names dropped from a peak in 2002 of 920 thousand to 580 thousand last year.

Among passenger cars, only Togliatti-based Lada sedans and Ulyanovsk-based UAZ off-road jeeps and SUVs have survived to this day. It’s important to keep in mind, however, that Lada still sells the top three most popular models in the country: the Priora (125 951), Granta (121 151) and Kalina (119 890).

Many local companies have entered production sharing agreements with global giants on their factory floors, leading to alliances like Ford-Sollers and Renault-Nissan-VAZ (VAZ, Russia’s leading domestic auto producer and owner of the Lada brand, is now majority owned by the Renault-Nissan alliance, which uses its facilities to both continue the Lada brand and assemble foreign vehicles).

In fact, the alliance announced in March plans to export its new economy-class Lada Granta sedan to Western markets like France and Slovenia to partially compensate for slumping domestic demand.

“I think the UAZ brand will also survive based on a joint platform with Ssang Young,” said UBS analyst Kirill Tachennikov.

Local truck producers have fared better, with Tatarstan-based KAMAZ (15 percent owned by Daimler and the European Bank for Reconstruction and Development) increasing sales by 19.4 percent in the first half of 2012 to $1.846 billion and Nizhny Novgorod-based GAZ group seeing profits increase 10.4 percent in the first half of last year thanks to a restructuring organized largely by ex-GM executive Bo Andersson.

The two producers have successfully competed with growing competition in the economic segment from Hyundai, Ford, Isuzu and lesser-known Chinese rivals.

Second Wave of Localization

The aim of the Russian government’s auto industry gambit has been to maximize local production and bring foreign technology within the country’s borders. “Although the current documents outlining state policy in the automobile industry don’t say this explicitly, one can clearly see between that lines that the aim is to localize assembly and reduce imports,” said Tachennikov.

The contracts signed between 2005 and 2007 had soft localization requirements (up to 30 percent) and low volumes (some as low as 25 thousand cars annually) and enabled foreign giants to test the Russian market.

Agreements in 2011 with Renault-Nissan, GM, Ford and Volkswagen have stipulated that local components are to reach 60 percent with an output of 300 thousand cars annually each. Thirty percent of foreign car brands produced in Russia are also to be equipped with Russian-produced engines and gearboxes.

In exchange, the companies have been promised duty-free import of components until July 1, 2018. This is no minor concession: Russia had negotiated hard with the WTO to maintain higher duties on new cars and busses (which are set to drop from 25 percent and 10 percent in 2012 to 15 percent and 5 percent by 2018, respectively).

As a result, the country’s auto components market grew by 8 percent last year (nearly double the overall level of economic growth) to his $41.8 billion.

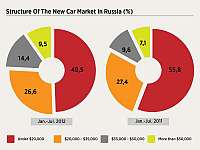

Market Saturation

While growth is expected to stabilize in the near future, Russia’s car market still stands to benefit from low saturation (250 cars per one thousand people versus 500 in Europe and 750 in the U.S.), currently high auto credit rates (15-17 percent annually) that are expected to drop and similarly dropping insurance costs (currently at 5-10 percent the cost of a car versus 3-5 percent in more developed markets).

“Insurance in Russia is very expensive because of the bad climate and poor roads,” said Litvinenko. “Financial services are also expensive because of the high cost of funding, but this situation is changing for the better. In the long-term I’d expect Russia’s market to become like the rest of Europe thanks to better roads and parking, which means the small and compact cars will win out.&rdquo

Russia’s Ministry of Industry and Trade predicts continued growth of the country’s car market to 4.17 million by 2020 (at that point, a full 3.75 million and expected to be produced in Russia); PricewaterhouseCoopers is more conservative at 3.5 million (still 20% more than today).

“In the last 20 years nearly every domestic passenger model – from the elite Volga to the Moskvich ‘people’s car’ – has stopped being produced,” said Sergei Udalov, Director of the Avtostat analytical agency. “But I’d expect the Lada brand to survive thanks to its low price. A difference of a few hundred dollars is still huge to the Russian buyer. But as the car will be increasingly assembled with Renault-Nissan parts, VAZ’s role will inevitably diminish.”

“Another trend, which is actually global, to keep an eye on is so-called ‘elite’ brands marketing smaller and cheaper models like the Audi Q3 and BMW X1. These are sure to be a big hit among Russia’s brand-obsessed consumers,” said Litvinenko.

Andrey Shkolin is Editor-in-Chief of web-site thinktwice.ru

All rights reserved by Rossiyskaya Gazeta.

Subscribe

to our newsletter!

Get the week's best stories straight to your inbox